The secret to success is to boost your profits by having visibility across your entire business. Here's four ways to do just that.

Let's be honest, running a construction business is no small feat. Between juggling job sites, managing crews, keeping clients happy, and somehow staying on top of the books, it's easy for money to quietly slip through the cracks. These "leaky profits" don't always show up on a balance sheet, which makes them especially sneaky. The good news? A few smart habits can go a long way toward sealing those leaks and keeping more of what you earn. Here are four areas worth focusing on.

1. Run your business more efficiently

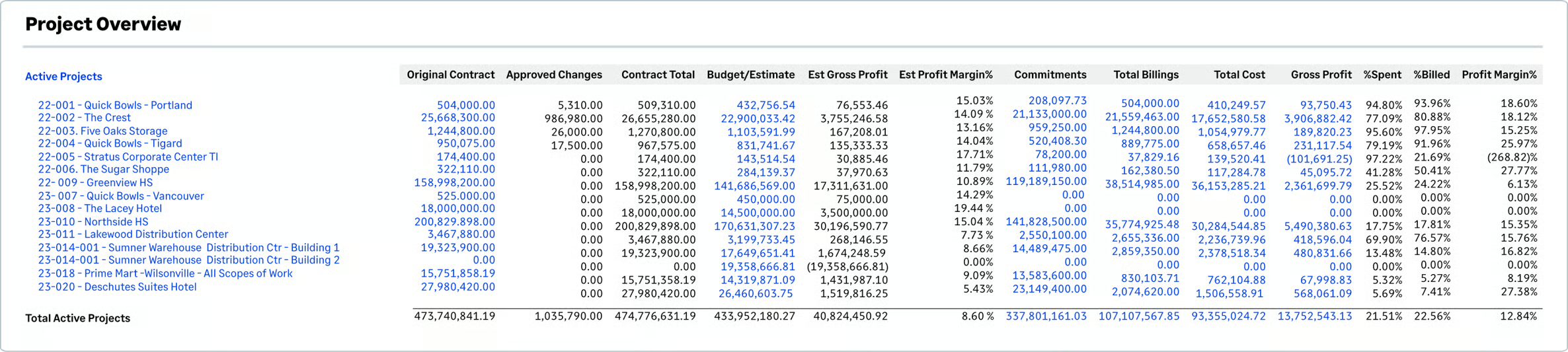

No matter how tight your operation, there's almost always room to tighten it up a little more. The trick is knowing where to look — and that's where key performance indicators (KPIs) come in. Think of KPIs as your business's vital signs: they help you spot red flags early, celebrate wins, and make smarter calls before small issues become big headaches.

If you're a contractor, client demands drive your most important project KPIs. At any given time, you should know whether your project is on schedule, on budget, and being performed safely and accurately. Here are some of the indicators worth keeping an eye on:

- Liquidity: Know how much cash you have available and drill down to the project level to see which projects are boosting your cash flow — and which ones are quietly draining it.

- Work backlog: Keep tabs on backlogged work so you can estimate future cash flow and adjust your plans accordingly. No more nasty surprises.

- Labor productivity: Labor is one of your biggest costs, so track it closely witch accurate time tracking: budgeted hours, hours worked, and percentage of work completed.

- Schedule adherence: Know where you stand on your project timeline so you can adjust quickly when delays or unexpected events pop up.

- Budget tracking: Monitor costs in real-time to catch budget issues early — before they snowball.

- Change requests: Proactively track, document, and negotiate payment for unplanned work. Surprises shouldn't cost you money.

- Project cash flow: Figure out which types of projects are generating cash and which are consuming it. Then do more of what works.

- Committed costs: Make sure suppliers and subcontractors are contractually committed to protect you from unnecessary risk.

2. Reap the benefits of automation

Keeping track of everything manually? That's a full-time job in itself, and an exhausting one at that. The good news is you don't have to do it alone. Automation tools can give you complete visibility into cash going in and out, and alert you the moment something looks off.

Automation also takes the grunt work out of essential finance functions like payroll, expense management, bank reconciliation, accounts payable, accounts receivable, and compliance. Instead of hunting through spreadsheets for answers that may already be out of date, you'll get real-time alerts the moment a tracked event occurs, like a late invoice, straight to your email, desktop, or phone. That means you can jump on issues right away, before they start eating into your margins.

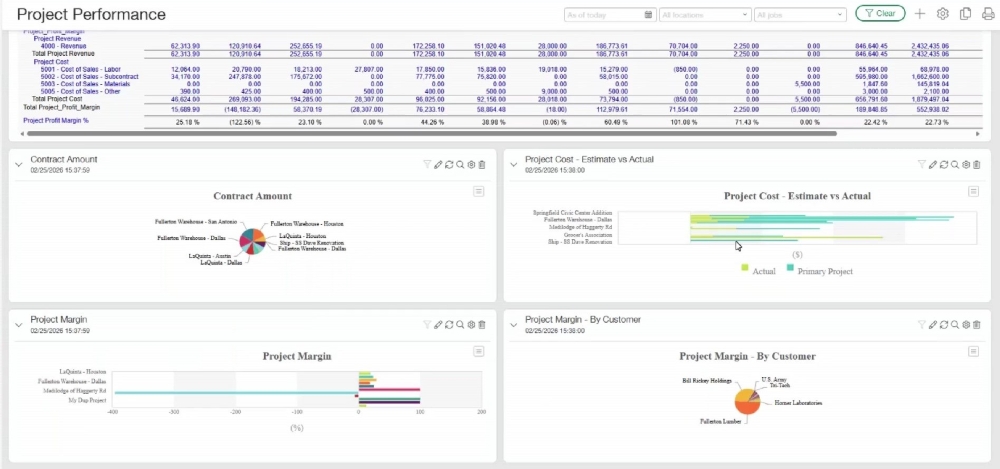

3. Create impactful reports

Are your reports actually doing their job? It's worth asking. If your team isn't using them, or worse, if the data in them is stale by the time anyone reads them — they're not helping anyone.

Ask for feedback. Tweak the content, formatting, or frequency as needed so your reports deliver real insight at the right time. Even better: pair your reports with a dashboard that pulls your key metrics, KPIs, and critical data into one clean, visual snapshot. Real-time dashboards mean no more guessing games about where your business stands.

The best dashboards are also customizable, different team members can see the data most relevant to their role, drill down for more detail, and generate their own reports without waiting on anyone else. This level of visibility is one of the reasons contractors are moving toward platforms like Sage Intacct Construction. Everyone stays informed, and decisions get made faster.

4. Give accurate estimates

Estimating is one of the hardest parts of the job, and one of the most important. A bad estimate here and there might seem manageable, but if you keep winning work that isn't actually profitable, things add up fast.

Start by being strategic about which jobs you bid on. It's tempting to throw your hat in the ring for everything, but spreading yourself thin across bids you're unlikely to win just wastes time and resources. Instead, focus on the types of projects where you consistently do well and make money, and bid smart to win more of those opportunities.

Technology can be a game-changer here. Financial and project management tools give you a much clearer picture of your true project costs, so your bids aren't just competitive, they're profitable. You'll win the right work at the right price, with a comfortable margin built in.

Shore up your finances strategically

You can't predict every curveball. But the more visibility you have across your business; in efficiency, automation, reporting, and estimating, the better equipped you'll be to handle whatever comes your way. Start making improvements in these four areas today, and you'll be well on your way to a tighter, more profitable business.

Want to see how this works in practice?

Take a self-guided product tour and explore how Sage Intacct Construction can support your team.

The right foundation for your next stage of growth

Our team of experts is here to help guide you every step of the way. Let’s start your ERP journey today!